Corporate Performance and resilience in a high inflation environment - remarks by Vasileios Madouros, Deputy Governor, Monetary and Financial Stability

29 June 2023

Speech

Good afternoon and thank you for joining us today at the Central Bank of Ireland.1

This is the third year running that we have worked with the ESRI and the European Investment Bank to host this conference.

Let me take this opportunity to thank both institutions for their continued collaboration.

While we each have different mandates and bring different perspectives, one thing unites us: serving the public good.

We do this partly through the analysis and research that our institutions conduct, which are a critical enabler of good policymaking.

Of course, analytical insights need to be complemented by insights from practical experience.

Which is why a core element of the Central Bank’s strategy is to be open and engaged.

Today’s event is a good example of that.

It aims to bring together researchers, policymakers and practitioners to help advance our collective understanding of the economy and the challenges and opportunities faced by the corporate sector.

The economic backdrop

Our event today relates to economic resilience, with a particular focus on the domestic business sector.

But, before focusing specifically on companies, let me share our latest assessment of the state of the Irish economy.

The global and Irish economies have been hit by a number of interlocking shocks in recent years, including the pandemic, Russia’s war against Ukraine and the ensuing energy crisis.

These shocks resulted in an imbalance between demand and supply across the global economy, which – in turn – led to accelerating price growth.

Last year, inflation in a number of countries around the world reached levels not seen in decades.

While headline inflation has fallen recently, as the energy crisis has receded, it remains far in excess of central banks’ targets, and measures of underlying inflation globally have been more persistent.

In response to growing inflationary pressures, the ECB’s Governing Council – like a number of central banks globally – has been raising interest rates to ensure a timely return of inflation to its 2% target.

In its most recent meeting, the Governing Council announced a further 25 basis point interest rate increase, which means interest rates have now risen by 400 basis points over the past year.

The magnitude and speed of these interest rate increases have been unparalleled in the euro area’s history, reflecting the magnitude and speed of the underlying shocks that have given rise to inflationary pressures.

Turning to economic activity in Ireland, this has proved resilient to date and, indeed, our assessment is that the economy is now operating at capacity.

This is most obvious in the labour market, where we have seen unemployment fall to its lowest level in more than two decades, employment having reached record highs and vacancies remaining at historically elevated levels.

While the full economic effects of the monetary policy tightening cycle still lie ahead, and the outlook remains uncertain, our latest assessment is that the expansion of the Irish economy is set to continue.

Our latest macroeconomic projections published last week expect modified domestic demand to grow by 3.7 per cent in 2023, followed by 2.5 per cent in both 2024 and 2025.2

Given the capacity constraints that we are already seeing in the economy, we are becoming increasingly attendant to the risk that overheating dynamics could emerge.

In that context, and as Ireland is part of a monetary union, fiscal policy also has an important role to play in guarding again the risk of overheating.

Charting a course for fiscal policy that does not exacerbate the imbalance between demand and supply conditions in the near term will be important.3

Business response to input cost inflation

Now let me turn to the corporate sector in particular.

At the Central Bank, we continuously seek to understand the prospects for, and risks around, the performance of the corporate sector as a whole.

It goes without saying that this is critical from the perspective of our price stability and economic advice mandates.

The collective decisions of individual businesses, whether in terms of investment, employment or pricing have important macroeconomic implications.

The corporate sector is also critical from the perspective of our financial stability mandate.

The financial sector provides core services to businesses across the country, so a resilient financial system is an essential precondition for a sustainable business environment.

And the financial sector is exposed to businesses through credit provision, so the performance of the corporate sector as whole is an important component of our financial stability assessment.

Over the past year, our focus has been on understanding how companies, large and small, have been affected by the rapid increase in input costs, whether it is energy or other critical inputs to production.

It is fair to say that we have been surprised by developments over the past year.

This time last year, we were flagging potential risks to domestic companies’ financial performance stemming from the large increase in input costs.

Developments over this period, however, suggest that the trading performance of Irish businesses has proved resilient in the face of significant input cost inflation.4

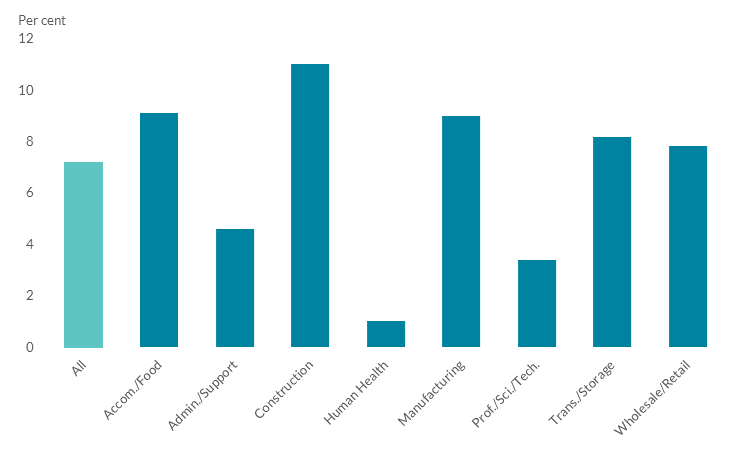

Turnover levels increased during 2022 and firms have generally passed on – or, in some cases, more than passed on – cost increases to customers (Chart 1).

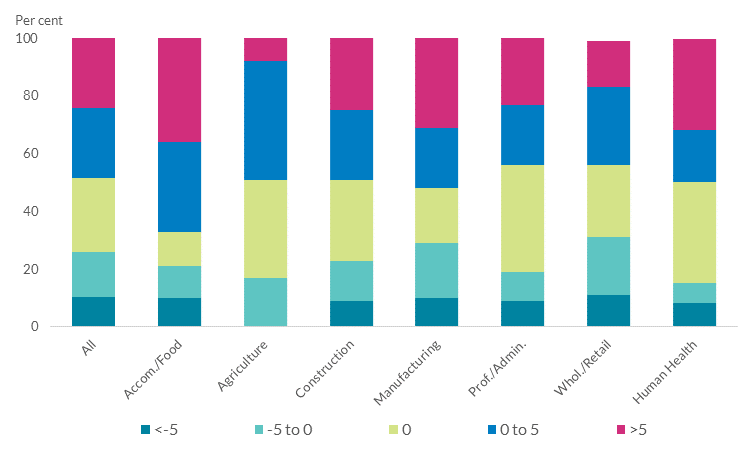

Indeed, survey evidence suggests that profit margins for SMEs either remained broadly stable or increased over the course of 2022 (Chart 2).

Chart 1: SMEs raised prices significantly during 2022

Source: Adhikari and McGeever (2023) (PDF 361.92KB)

Notes: Average unit price change between March 2022 and September 2022 by sector.

Chart 2: Most SMEs’ gross profit margins remained stable or increased during

2022

Source: Adhikari and McGeever (2023) (PDF 361.92KB)

Notes: The share of SMEs by percentage point change in gross profit margin by sector.

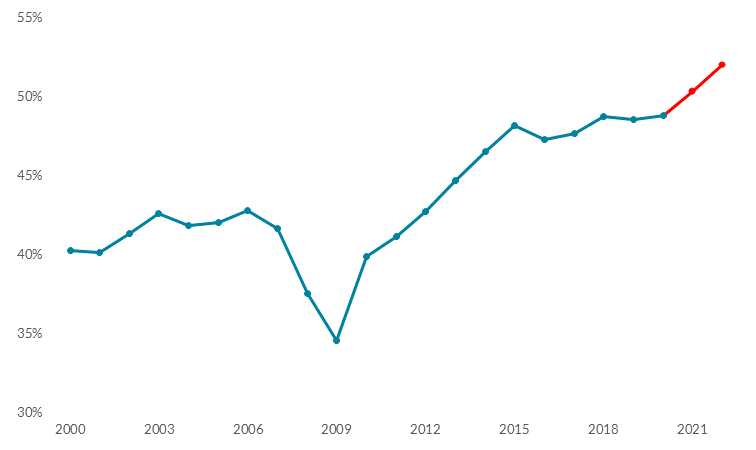

Similarly, aggregate data point to increases in unit profits by the domestic corporate sector as a whole, as well as different industries within that, with an associated increase in the profit share (Chart 3).

But there’s another side to this coin. The increase in profitability observed last year contributed to broader inflationary pressures across the economy.

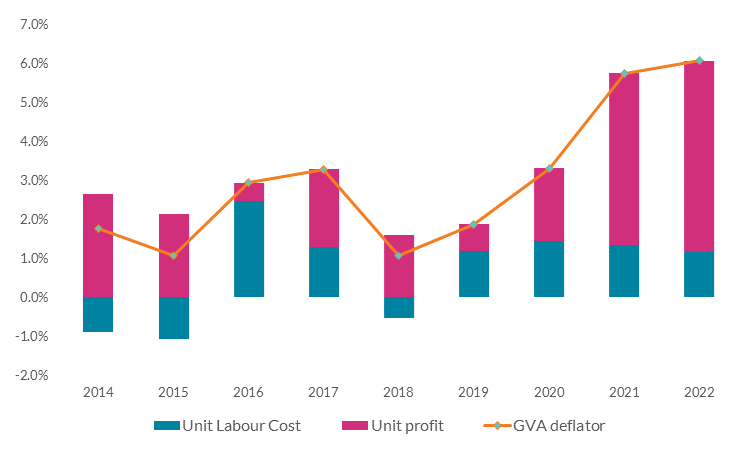

Indeed, if we look at a decomposition of the contribution to inflation from goods and services produced in Ireland, excluding sectors dominated by MNE activity, it suggests that – at an aggregate level – the increase in unit profits was a more important factor than increases in unit labour costs as a driver of inflation (Chart 4).

Chart 3: Profit share across the domestically-oriented corporate sector

Source: CSO

Notes: The “domestic” sectors exclude those whose output is dominated by foreign-owned MNEs.

Chart 4: Decomposition of changes in the GVA deflator for domestically-oriented sectors

Source: CSO

Notes: The “domestic” sectors exclude those whose output is dominated by foreign-owned MNEs. GVA at basic prices, which does not include taxes or subsidies on products, is used for the purposes of this chart, as such taxes and subsidies are not sectorised in the National Accounts and cannot be attributed to just the domestic sectors.

Looking ahead

Let me know turn to the outlook for the corporate sector.

As I mentioned earlier, the Governing Council of the ECB has increased interest rates by around 400bps since last summer.

Given the long and variable lags associated with the transmission of monetary policy to the broader economy, the full economic effects of the tightening cycle still lie ahead of us.

What does this mean for businesses?

Most immediately, the tightening of financial conditions will have implications for the cost and availability of credit for businesses.

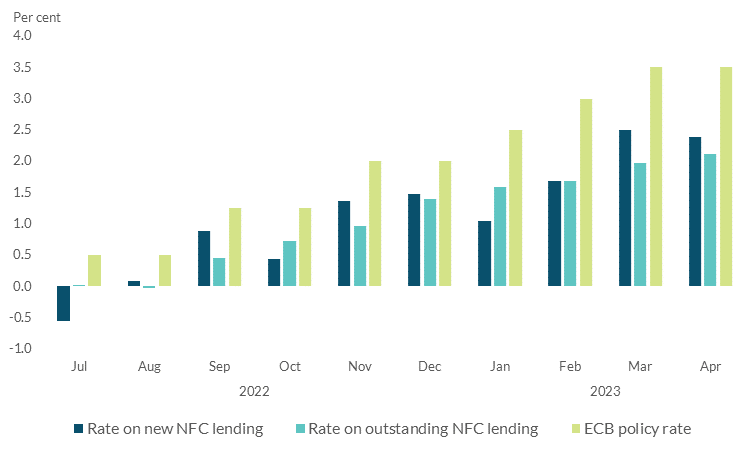

Indeed, interest rates on new business lending have risen significantly since mid-2022 (Chart 5).

We have also already seen a moderation in new lending to companies over the past year.

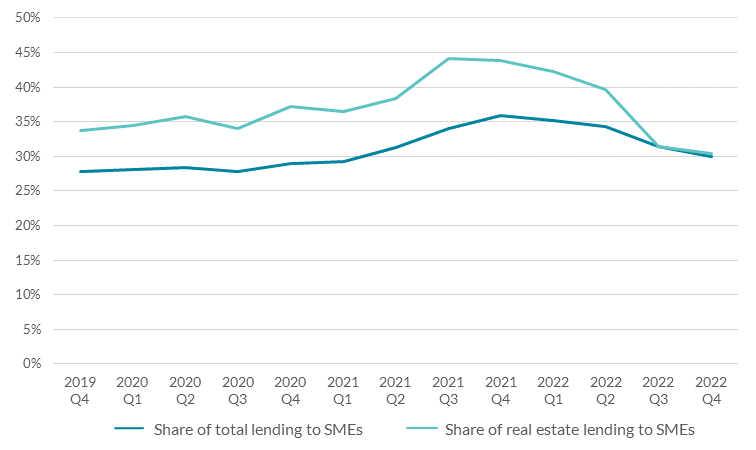

This has been particularly evident in terms of credit provision by non-bank lenders and, within that, non-bank lending advanced to SMEs for real estate activities (Chart 6).

Chart 5: Interest rates on new business loans have risen significantly

Source: Central Bank of Ireland

Notes: Interest rates on new bank lending to non-financial corporations and deposit accounts with agreed maturities. See Table B.2.1 of the Central Bank of Ireland’s Retail Interest Rates statistics.

Chart 6: The share of lending provided by non-banks contracted through

2022

Source: Central Bank of Ireland; Central Credit Register.

Notes: The share of new lending to Irish SMEs originated by non-banks, presented as a four-quarter moving average. ‘Total lending’ refers to borrowing from all non-financial SMEs. ‘Real estate lending’ refers to borrowing from SMEs engaged in construction and real estate activities.

In that context, the resilience of SMEs to this tightening cycle is supported by the significant lowering of indebtedness of Irish businesses since the 2008 crisis.

For example, only around half of SMEs have any form of debt. And the level of outstanding bank debt owed by the SME sector has fallen by approximately two thirds since 2008.

This limits the underlying vulnerability of the SME sector as a whole to the direct effects of higher interest rates, relative to the past.

Beyond the direct effects on financing costs, tighter monetary policy will also result in a dampening of demand conditions across the economy.

This is necessary to bring inflation back to 2%.

Ultimately, developments in business profitability observed recently point to the strength in demand conditions across the economy, relative to constrained supply.

This has allowed firms to maintain, or even increase, profit margins in the face of the large input cost shock.

Wages have grown more slowly than profits over this period, but are expected to pick up this year and next. This reflects some degree of real wage catch-up following the initial inflation shock.

Achieving a slowing in the rate of inflation, while real wages recover some of their losses, will require that the balance of demand and supply conditions across the economy does not enable the very fast increases in unit profits seen most recently.

Again, this underpins the importance that both monetary and fiscal policies are set to ensure that demand and supply conditions across the economy are balanced.

Conclusion

Let me conclude.

To date, we have observed that businesses have largely been able pass on input price increases to their consumers and maintain, or even increase, margins.

This has added to inflationary pressures and points to the strength of underlying demand conditions in the economy.

As the impact of monetary policy tightening transmits through the economy in the months ahead, it will be important that businesses are prepared for a moderation in demand growth.

Irish SMEs have been in a long-running deleveraging cycle, which means that – in the face of rising interest rates – the SME sector is in a better starting point from a resilience perspective.

These issues will remain at the forefront of our own focus at the Central Bank, as the economy continues its adjustment to a very different macro-financial environment than the one that prevailed over the past decade.

Let me will now hand over to my colleague, Ricardo Mourinho. I hope you have a productive conference this afternoon

[1] I am grateful to Mark Cassidy, Patrick Haran, Rob Kelly, Fergal McCann, Niall McGeever and Martin O’Brien, for their advice, comments and assistance in preparing these remarks.

[2] See Quarterly Bulletin, June 2023 (PDF 3.11MB).

[3] See Conefrey et al (2023), ‘Managing the Public Finances in a Full-Employment Economy’.

[4] See Adhikari and McGeever (2023) ‘How Resilient Are Irish SMEs to Input Cost Inflation?’ and Financial Stability Review, June 2023 (PDF 1.23MB).